The $7 Patent Stock That Runs Like a Hedge Fund

Immersion Corp is sitting on $11/share in value, quietly buying back stock, and betting big on a misunderstood turnaround.

I typically avoid complex investments. But occasionally, the complexity hides value—if the right management is at the helm. Immersion Corporation (IMMR) is one of those rare cases.

At it’s heart IMMR is a hedge fund with a cash flowing IP portfolio. The fund that seems to be well managed, and value focused. The company is trading at a 30-40% discount to it’s Sum of The Parts Value. On top of that, IMMR’s largest position is in BNED 0.00%↑, one of the picks I shared with you earlier.

Think of IMMR as Pershing Square without the fees—a microcap with owner-operator discipline, a fortress balance sheet, and a discounted portfolio of high-conviction bets.

Let’s Break it down.

Investment Portfolio

IMMR isn’t just a licensing business—it’s also a stealth investment vehicle. As of the latest 13-F, the company holds $184M in public equities, primarily in Barnes & Noble Education (BNED), where it now holds a controlling stake and board representation. The complexity from consolidating BNED’s financials has scared off most analysts—creating opportunity.

Cash and Debt

IMMR holds $85M in Cash and only $7M in LT debt.

Adding these two pieces together we’re at $262M in Net Asset value. That’s $8 in per share NAV on the balance sheet, for a stock that today trades at $7.55. But wait there’s more!

Operating IP business

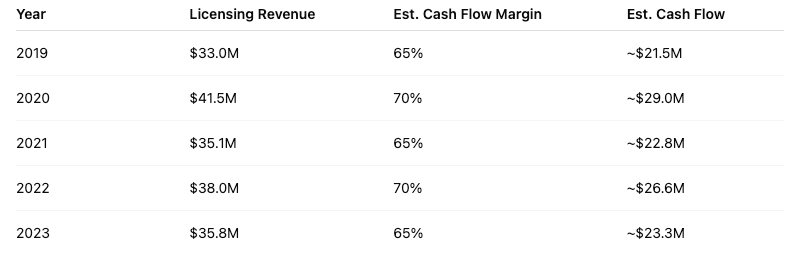

Imagine you invent the "rumble" in PlayStation controllers. Now imagine every major gaming or smartphone OEM pays you to use it. That’s IMMR’s IP model: a portfolio of over 1,200 patents in haptics, proven in court, and monetized through licensing. This machine throws off ~$25M in annual cash flow—with minimal overhead.

IMMR has a portfolio of 1200+ patents in the haptic technology. Major Consumer electronic companies pay them for use of these technologies. The patents have been proven in court numerous times and most of them go out to 2034, and many further than that.

Furthermore we can look forward to see a pipeline of upcoming renewals for larger deals announced previously.

At the same time some of the more lucrative haptics patents that IMMR has will expire between 2026 and 2033 unless they are able to extend these.

Expiration Timeline for IMMR’s Core IP

1. Gaming & Consumer Electronics Patents

Filed: 2005–2011 (e.g., DualShock haptics, force feedback in controllers)

Expires: 2025–2031

Impact: High — these patents support deals with Sony (PlayStation) and Meta (Oculus/Quest)

2. Mobile Device Haptics

Filed: 2006–2013

Expires: 2026–2033

Impact: Very High — these patents underlie licensing to Samsung, which accounts for a major portion of historical revenue

3. Automotive Interface Patents

Filed: 2012–2018

Expires: 2032–2038

Impact: Medium — important for long-term growth, but currently less revenue-heavy

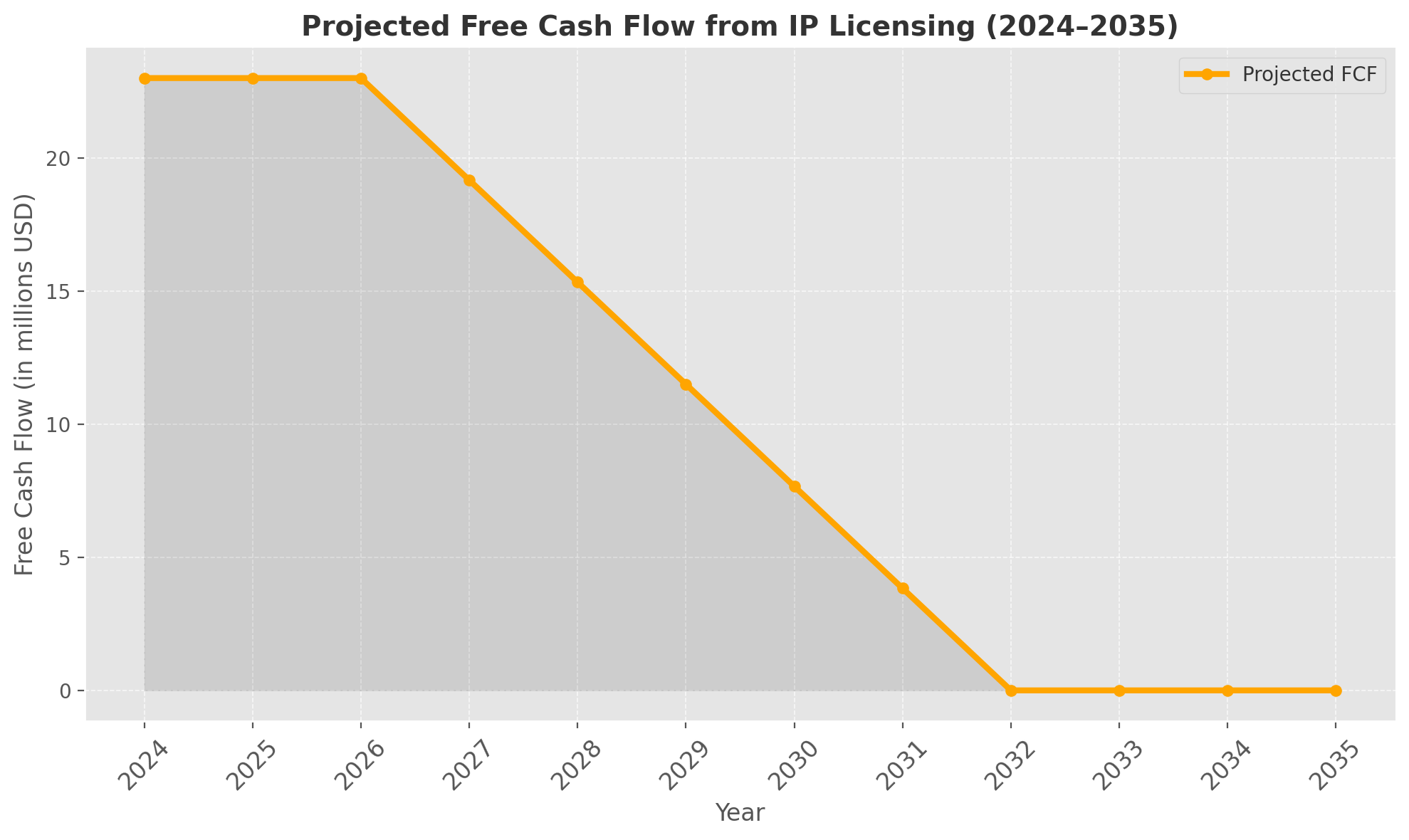

If I assume that there is no extension and we continue at minimal margins w/ no further IP wins after the expiration of these contracts (extremely conservative), I get the following Projected FCF curve:

Using this base we can come to a base case valuation for the IP business:

NPV: $97.4 million

Shares Outstanding: 33 million

→ NPV per share = $97.4M ÷ 33M = $2.95/share

So, the IP business alone is worth approximately $2.95 per share today on a DCF basis, assuming key patents expire by 2032 and a 12% discount rate.

Add the $2.95/share from IP to the $8/share in cash and investments, and you get $11.04 in intrinsic value. At today’s price of $7.55, the stock trades at a 30% discount. That’s before giving credit to any upside from BNED.

But before we get too excited, let’s make sure management isn’t going to screw us.

Management Alignment

CEO Eric Singer is the kind of capital allocator you want in a complex setup. He takes a $160K salary, owns $19M in stock, and has cut headcount to 9 people while repurchasing shares at below intrinsic value. He’s running IMMR like a lean fund—not a traditional operating company.

Some notable MGMT actions:

Transitioned to Pure-play Licensing Model:

Headcount reduced to approximately 9 full-time employees by 2023

R&D expenses cut to near-zero (from over $10M/year pre-2019)

SG&A expenses fell from ~$17M in 2017 to ~$5M–$7M range recently

Litigation and licensing enforcement are now outsourced to specialists, reducing fixed costs

IMMR Share Repurchase:

3.4 million shares in FY 2022 - $6.24/ share

2.6 million shares in FY 2023 - $7.55/ share

These buybacks were done below what I would consider intrinsic value here.

Did issue shares to buy controlling BNED, instead of paying out in cash, as managment saw deep value in the investment:

“We identified BNED as a severely undervalued public company with long-term assets and operating leverage that can benefit from strategic support, capital, and patience. By issuing shares to acquire a majority stake, we maintain balance sheet strength while gaining a seat at the table in a potentially attractive special situation.”

Risks

BNED underperformance: the thesis leans heavily on this turnaround. (see my earlier writeup)

Patent expirations: post-2030, core licensing cash flow may decline sharply unless the portfolio is refreshed.

Management execution: the strategy depends on disciplined capital allocation. Any deviation could impair returns.

IMMR isn’t your typical tech stock. It’s quiet, cash-rich, undervalued, and owner-operated. It may not scale, but it doesn’t have to. At today’s price, you’re buying a hedge-fund-like asset base with a cash-flowing IP stream—for a 30% discount.

Any idea what they've been issuing debt for? Debt ballooned in 2025 for some reason.

Thanks for the write-up, I looked at them a year ago and decided to wait… you triggered me to look into them again.

A comment: the IMMR Cash and Debt section seems to be based on April 2024 data instead of January, 2025 - or am I misreading sth?